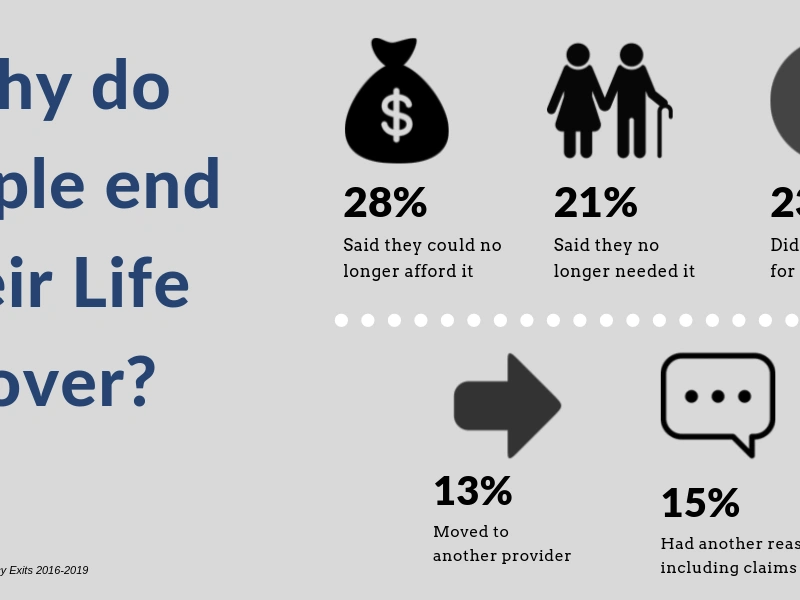

With people expecting to live longer, often it's not cover for if they die that they're looking for but cover for if they get seriously ill. This kind of insurance is called critical illness or trauma insurance. It's different from health insurance, which will pay for medical care, such as diagnostics or surgery; critical illness insurance will pay out a lump sum.

Late last year, Gen Re published the findings from their 8th 'Dread Disease' survey. The survey looks at the experience in China, Hong Kong, Malaysia and Singapore of 39 companies covering Dread Diseases from 2015 to 2019. A dread disease is a disease:

- with a significant impact on lifestyle (e.g. multiple sclerosis)

- with a significant impact on longevity (e.g. cancer),

- which incurs high costs (e.g. extensive burns, persistent vegetative state), and/or

- may cause significant and permanent residual morbidity (loss of eyes or limbs).

The survey found that over time more and more conditions are being covered. The maximum number of conditions covered in 2019 was 168!

The survey also found that only 5% of conditions covered had significant numbers of claims. This means that people are paying more for their policy to include conditions that they are highly unlikely to claim on. 76% of conditions covered had zero or a negligible number of claims during the study period.

Critical Illness cover aims to cover conditions that may not kill you but are likely to have a severe financial impact. It includes the kinds of diseases and illnesses described by the 'dread disease' definition.

In considering Critical Illness cover, you need to balance the cost of the policy with the likelihood of actually getting the condition. For example, our CEO, Gillian Vaughan, recalls that at one time, one NZ provider covered Variant Creutzfeldt-Jakob Disease (mad cow disease), even though there has never been a case here.

The diagnosis and severity of deadly illnesses have changed significantly with medical and technological advancements. For example, some cancers can now be considered minor, with a survival rate of 100%, and some illnesses that were once considered deadly have such effective treatments that we scarcely hear about them in NZ, such as AIDS.

When comparing providers and policies, you should consider these kinds of things. Paying more for a policy that covers more conditions may not be the best fit for you. You should also carefully read the definitions and under what circumstances the provider will payout, as these can vary considerably.

Pinnacle Life first offered Serious Illness Cover in 2008. It was the first time this kind of cover was available to buy online, fully underwritten. Serious Illness covered four serious conditions: heart attack, cancer, stroke, and heart bypass surgery. Pinnacle Life would pay out a lump sum if you suffered from any of these. We still have customers with this product.

Over time our customers wanted a product that would cover more than four conditions, so we introduced Critical Illness. Critical Illness covers 24 conditions, as well as the four listed above, including Alzheimer's, Multiple Sclerosis, and Parkinson's.

24 conditions is clearly on the low side of the number of conditions covered by Asian providers. This is intentional. We aim to provide customers with good value cover. We believe it's important to have cover for the things that are more likely to happen and pay a reasonable premium than to have cover for every possible eventuality and pay more. Sometimes, more is not better.